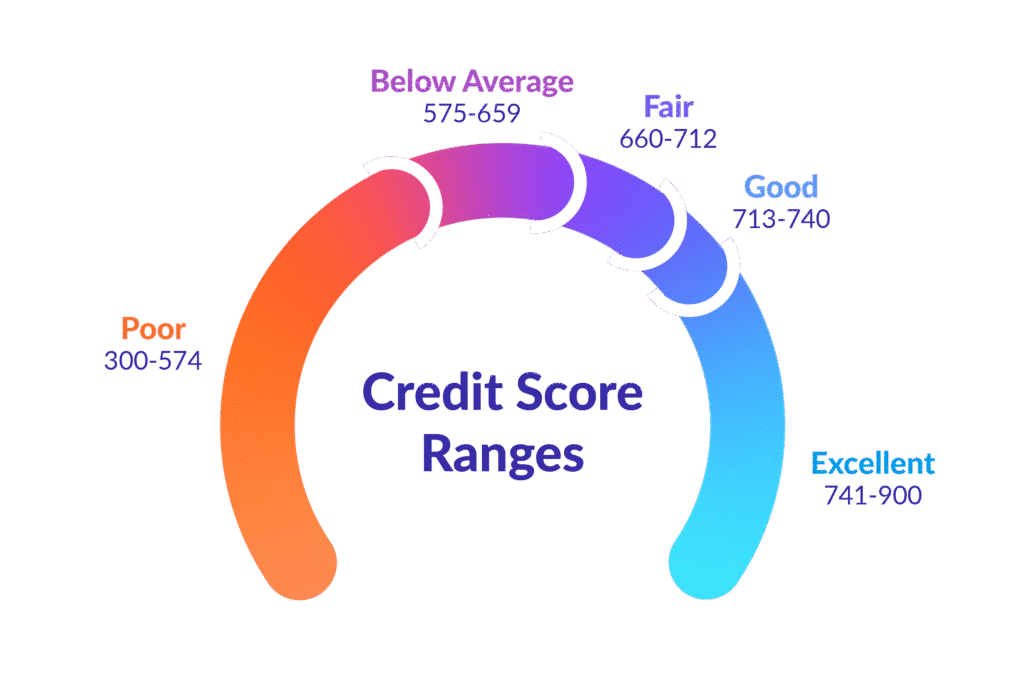

300 to 650

Any score lower than 650* is generally considered "fair” or “below average"

Credit scores below 650 are often categorized by lenders as “fair” or “below average.” People in this range may face stricter lending criteria depending on the lender’s policies. Credit decisions vary, and each lender uses its own standards when evaluating applications.

Our proven process can help you to fix your creditOur process is designed to guide and educate you about your credit profile, helping you understand your report and make informed decisions.

Analyze

We work with you to review your credit reports and highlight items that may require attention, including late payments, collections, and other factors.

Guidance & Education

We provide explanations and recommendations on how to understand your credit reports and potential next steps for addressing items of concern.

Monitor

We help you stay informed about changes to your credit reports and provide ongoing guidance so you can make confident, informed financial decisions over time.

The timeline varies for each individual and depends on their credit profile. Our process focuses on providing guidance, education, and support so clients can make informed decisions about their credit. Every situation is unique, and improvements can occur at different rates depending on individual circumstances.

Building good credit takes time and consistent financial responsibilityyour headingThere is no specific timeline for establishing good credit because it depends on various factors, including your starting point and your financial habits. Here are some key considerations:

01 Credit Score Basics:

Your credit score is a numerical representation of your creditworthiness. 300 to 900. Generally, a good credit score is considered to be above 700.

02 Timely Payments:

Making on-time payments for your credit accounts, such as credit cards, loans, and bills, is crucial for building good credit. Payment history accounts for a significant portion of your credit score.

03 Credit Utilization:

Keep your credit card balances low in relation to your credit limits. A lower credit utilization ratio (credit card balance compared to credit limit) is better for your credit score.

04 Credit Mix:

Having a mix of different types of credit, such as credit cards, installment loans (e.g., auto loans or mortgages), and retail accounts, can positively impact your credit score.

05 Length of Credit History:

The age of your credit accounts matters. Generally, the longer your credit history, the better. This is why it takes time to build a good credit history.

06 New Credit Inquiries:

Applying for too much new credit in a short period can have a negative impact on your credit score, so be cautious when opening new accounts.

07 Negative Information:

Negative items like late payments, collections, and bankruptcies can significantly harm your credit. These may stay on your credit report for several years.

Contact Us

Fill in your details and send us a message. Our team will reach out shortly to guide you with the next steps.